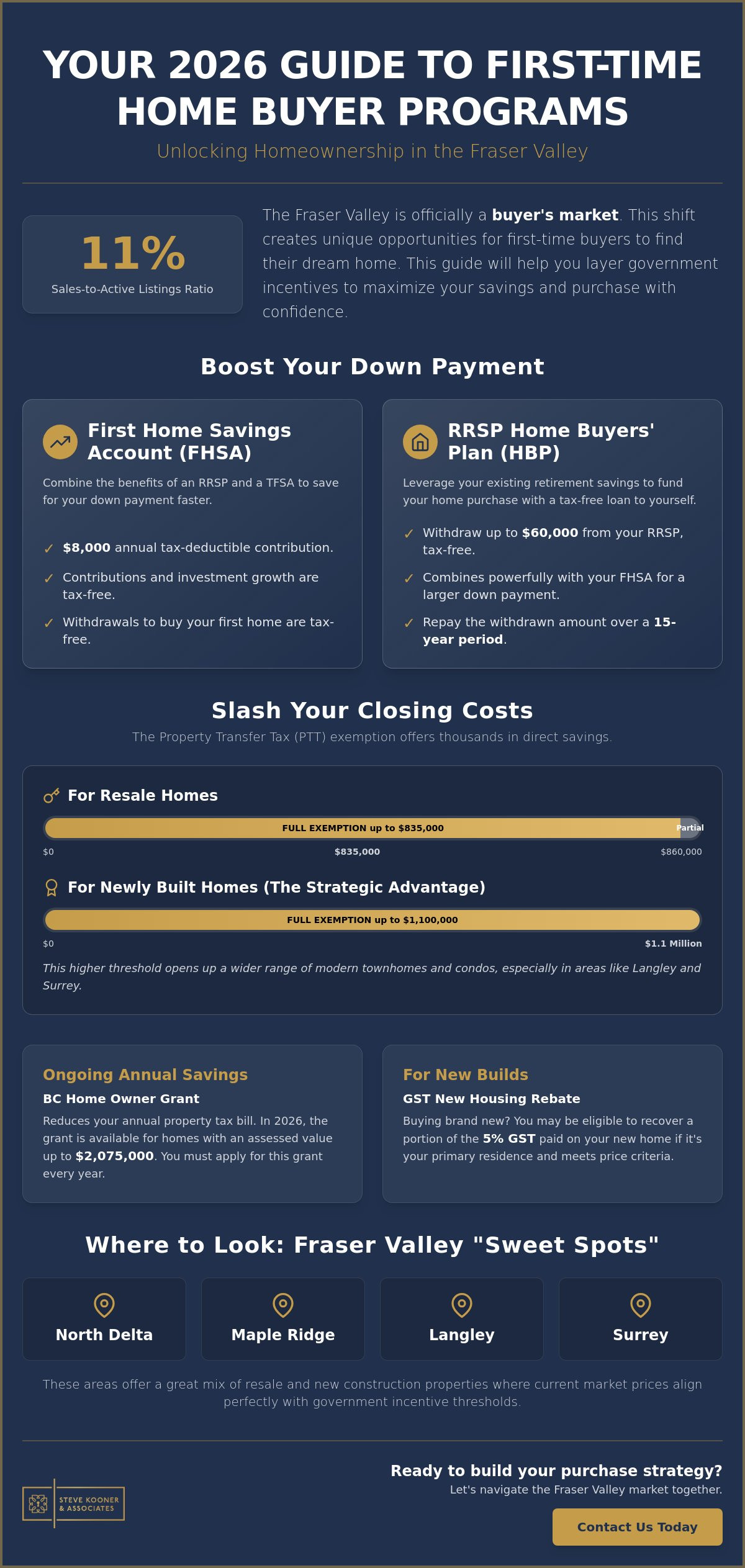

Did you know that with a sales-to-active listings ratio of just 11%, the Fraser Valley has officially shifted into a buyer's market for 2026? While benchmark prices have dipped, the stress of high down payment requirements and the confusion over first time home buyer BC programs still keep many people on the sidelines. It's completely normal to feel stuck between wanting a home and worrying about the financial fine print, but you don't have to figure it out alone.

We're here to help you move forward with clarity and confidence. This guide will show you exactly how to master the latest incentives so you can maximize your savings and strategically layer your benefits. You'll learn how to combine the $835,000 property transfer tax exemption with the updated $60,000 RRSP withdrawal limit to lower your entry costs. We'll provide a clear breakdown of every 2026 provincial benefit and show you how to apply them to the unique opportunities currently found across the Fraser Valley landscape.

Key Takeaways

- Learn how to qualify for a full Property Transfer Tax exemption on homes up to $835,000 to significantly reduce your upfront closing costs.

- Discover the strategic advantage of buying new construction in Langley or Surrey to access higher tax exemption thresholds up to $1.1 million.

- Understand how to maximize your down payment by combining the 2026 FHSA rules with the increased $60,000 RRSP withdrawal limit.

- Identify the specific "sweet spot" neighborhoods in North Delta and Maple Ridge where current market prices align best with available government incentives.

- Master the process of layering various first time home buyer BC programs to build a confident and successful purchase strategy in a buyer's market.

Essential 2026 BC First Time Home Buyer Programs

Buying your first home in the Fraser Valley is a major milestone, and we want to make sure you're taking advantage of every dollar available to you. To qualify for most first time home buyer BC programs, you must be a Canadian citizen or permanent resident who has lived in BC for at least 12 consecutive months before the date you register the property. You also cannot have owned a principal residence anywhere in the world at any time. It's about more than just checking boxes; it's about building a foundation for your future in a community you love.

To better understand how these programs work together to maximize your savings, watch this helpful video:

Strategic saving starts with federal tools like the First Home Savings Account (FHSA). This account allows you to contribute up to $8,000 annually with tax-deductible contributions and tax-free withdrawals. You can pair this with the RRSP Home Buyers' Plan, which allows you to withdraw up to $60,000 from your RRSP. This combination gives you a powerful head start on your down payment in neighborhoods like North Delta or Langley. Just remember that HBP withdrawals must be paid back into your RRSP over a 15 year period to avoid tax penalties.

Property Transfer Tax (PTT) Exemptions in 2026

The PTT exemption is a direct closing cost saving for BC residents that can keep thousands of dollars in your pocket. For 2026, you'll receive a full exemption on homes with a fair market value of $835,000 or less. If your home is priced between $835,001 and $860,000, you'll still receive a partial exemption. If you're buying with a partner who isn't a first-time buyer, you can still claim an exemption based on your percentage of ownership. This is one of the most effective first time home buyer BC programs for reducing the cash you need on closing day.

The BC Home Owner Grant

Once you've moved into your new home, the savings continue. The BC Home Owner Grant reduces the amount of property tax you pay each year on your principal residence. For 2026, the threshold for this grant is a property value of $2,075,000, which covers the vast majority of homes in the Fraser Valley. You must remember to apply for this grant every single year through the provincial website to keep your monthly carrying costs low. You can use our Mortgage Calculator to see how these annual savings impact your total budget and monthly affordability.

Strategic Incentives for New Construction and Presales

While the standard BC Property Transfer Tax Exemption is a fantastic tool for resale homes, the real strategic win often lies in new construction. In growing hubs like Langley and Surrey, first-time buyers can tap into the Newly Built Home Exemption. This program offers a full PTT exemption on homes valued up to $1,100,000, which is a much higher ceiling than the resale limit. It's a game changer among first time home buyer BC programs because it opens up a wider range of modern townhomes and condos that would otherwise trigger heavy closing costs.

Navigating the GST New Housing Rebate

Buying brand new involves GST, but you don't always have to shoulder the full 5% tax. The GST New Housing Rebate allows you to recover a portion of the tax paid if the home is your primary residence and meets specific price points. In many Fraser Valley presale contracts, developers use "GST-inclusive" pricing, which means the rebate is already factored into your purchase price to simplify your financing. You can explore current developments to see which new homes in our region qualify for these significant tax savings.

Presale Strategies for First-Time Buyers

Presales offer a unique timeline advantage that's perfect if you're still building your savings. You lock in 2026 pricing today but won't take on a mortgage until the building is complete, often 18 to 36 months down the road. This window gives you extra time to grow your down payment while your future home potentially appreciates. Many developers offer tiered deposit structures, allowing you to pay your 10% or 15% deposit in smaller increments over several months. To navigate these contracts safely, it's vital to work with a partner who understands real estate project sales and can secure early access to the best floor plans.

By layering these incentives, you aren't just buying a property; you're executing a sophisticated financial plan. You save on PTT through the newly built exemption and reduce your tax burden via the GST rebate, all while using a presale timeline to maximize your financial readiness. If you're ready to see how these numbers apply to your budget, feel free to get in touch for a personalized strategy session.

Your Fraser Valley Homeownership Roadmap

Your journey to owning a home starts with a rigorous financial audit. With the Bank of Canada policy rate sitting at 2.25% as of June 2026, getting a solid pre-approval is your most important first move. This step ensures you're ready to leverage first time home buyer BC programs the moment the right property appears. You'll need to know exactly how the BC First Time Home Buyers' Program impacts your total cash flow before you start visiting open houses.

Identifying "sweet spot" neighborhoods is where your strategy truly meets your lifestyle. Langley, North Delta, and Maple Ridge remain prime targets for buyers in 2026. In these areas, townhomes have a benchmark price of $769,500, and condos sit around $533,000. These price points align perfectly with provincial tax exemptions, allowing you to maximize your savings while securing a high-quality property in a growing community.

Local Market Nuances: From Surrey to Abbotsford

Transit-oriented developments are the current gold standard for first-time buyers in the valley. The SkyTrain expansion through Surrey and into Langley is creating high-value pockets near future stations. While these areas offer great long-term potential, don't forget to budget for the hidden costs of buying a home in Abbotsford or Surrey. Even with government help, you'll still need to cover home inspections, legal fees, and property tax adjustments.

Why a Local Expert Matters

The Fraser Valley is currently a buyer's market with a sales-to-active listings ratio of 11%. This gives you more room to negotiate, but you still need a partner who can navigate the complex paperwork of first time home buyer BC programs. At Steve Kooner & Associates, we provide the personalized first-time buyer guidance you need to win in any market condition. We don't just find you a house; we build a strategic plan that protects your interests and sets you up for long-term financial success. Let's work together to turn these 2026 incentives into the keys to your new front door.

Take the Next Step Toward Your Fraser Valley Home

You now have the roadmap to navigate 2026 with confidence. By leveraging first time home buyer BC programs like the Property Transfer Tax exemption and the updated $60,000 HBP withdrawal limit, you can drastically reduce your financial barriers. Whether you're eyeing a presale in Langley or a condo in North Delta, the current buyer's market offers a unique window to build equity on your own terms. You've learned how to layer these incentives; now it's time to put that strategy into motion.

Our dedicated team at Royal LePage Wolstencroft Realty is here to ensure you don't miss a single opportunity. We specialize in Fraser Valley presale developments and provide comprehensive relocation and mortgage support for every step of your journey. We'll help you navigate the paperwork and the negotiations so you can focus on the excitement of your first move. Ready to move from dreaming to doing? Start your journey with our First-Time Buyer Guide and personalized consultation today. Your future home is closer than you think, and we're excited to help you find it.

Frequently Asked Questions

Can I use the BC First Time Home Buyers' Program for a presale condo?

Yes, you can receive an exemption for a presale condo, but it usually falls under the Newly Built Home Exemption. This specific branch of first time home buyer BC programs is ideal for the Fraser Valley because it offers a full Property Transfer Tax exemption on new homes valued up to $1,100,000. This higher limit makes brand new condos in areas like Surrey or Langley much more accessible for your first purchase.

What happens if my first home in the Fraser Valley costs more than the PTT exemption limit?

You may still qualify for a partial exemption if your home price is slightly above the $835,000 limit for resale properties. In 2026, the partial exemption applies to homes valued between $835,001 and $860,000. However, if the purchase price is $860,001 or higher, you'll need to pay the full Property Transfer Tax. It's a vital detail to discuss with your realtor during the offer writing stage to ensure your budget remains accurate.

Do I have to pay back the RRSP Home Buyers' Plan withdrawal?

You are required to repay the funds withdrawn from your RRSP through the Home Buyers' Plan over a 15 year window. Repayments start in the second year after your withdrawal, and you'll receive a notice from the CRA each year stating your required amount. If you fail to make a payment, that portion is considered taxable income for that year. It's a manageable way to borrow from yourself while keeping your long-term retirement goals on track.

Is the GST New Housing Rebate the same as the First Time Home Buyers' Program?

No, the GST New Housing Rebate and the First Time Home Buyers' Program are distinct incentives that target different taxes. The GST rebate is a federal program that refunds a portion of the 5% tax paid on new construction homes. In contrast, the provincial program focuses on reducing or eliminating the Property Transfer Tax. Understanding how to layer these first time home buyer BC programs is the key to maximizing your total savings on closing day.

Disclaimer

"Not intended to solicit buyers or sellers that are under current agency agreement" "Each RE/MAX office is independently owned and operated"