What if the biggest risk in the 2026 Fraser Valley market isn't the price you get, but the sequence you choose? You've likely spent nights wondering, "should I sell my home before buying a new one," while watching active listings climb to 9,816 across our region. It's a completely natural concern. The fear of missing out on your dream home while waiting for a buyer, or the anxiety of carrying two mortgages, can feel overwhelming. We know you want a transition that feels like a step forward, not a financial gamble.

You deserve a move that protects your equity and your peace of mind. In this guide, we'll master the timing of your next move with a strategic breakdown of selling versus buying first in the current BC market. We'll explore how the current 11 percent sales to active listings ratio gives you unique leverage. You'll learn how to use specific contract clauses and presale opportunities to ensure you win your next bid without overextending your budget.

Key Takeaways

- Gain clarity on how neighborhood-specific inventory in areas like Willoughby and Abbotsford shapes your optimal moving strategy.

- Evaluate the financial benefits of selling first to lock in your budget and eliminate the stress of carrying two mortgages.

- Master the strategic use of contract clauses to protect yourself if you're still weighing the question: should I sell my home before buying a new one?

- Discover how the presale market offers a strategic "third way" to bridge the gap between your current home and your next chapter.

- Access a professional five-step action plan to calculate your buying power and navigate the transition with total confidence.

Should You Sell Your Home Before Buying? The 2026 Market Reality

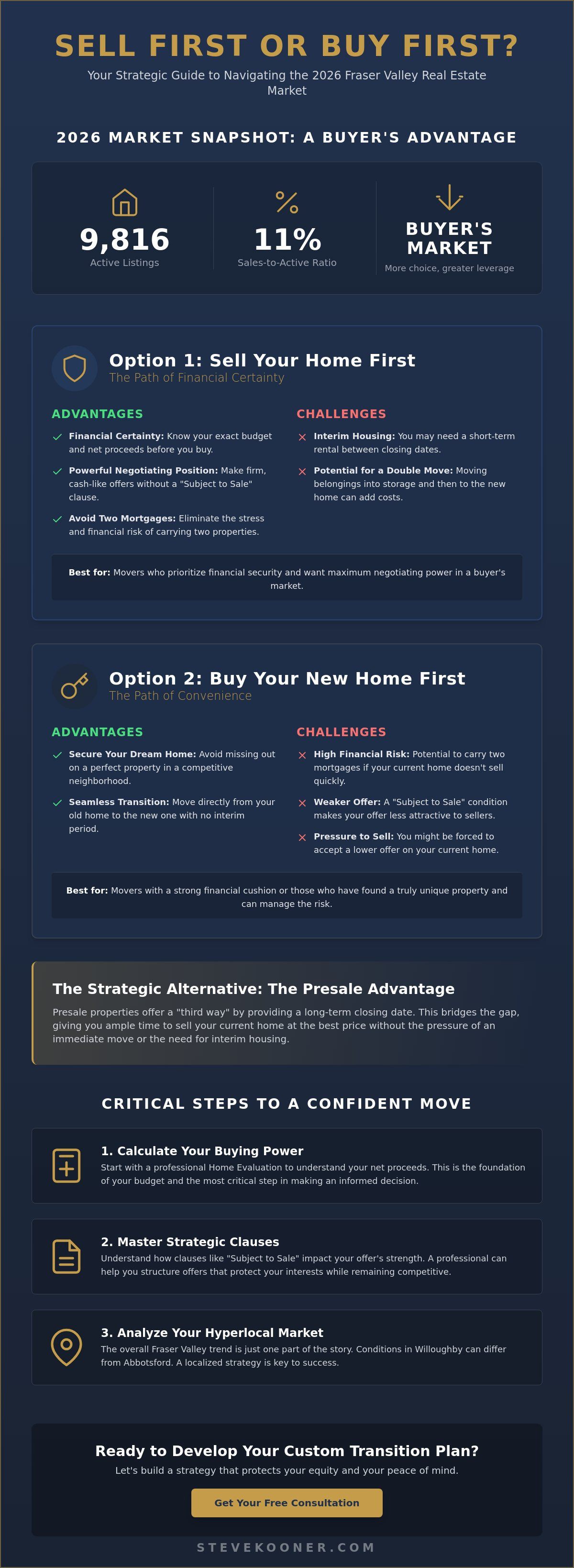

Deciding the order of your move is more than a logistical hurdle. It's a strategic choice that defines your financial safety net. In the current 2026 Fraser Valley market, we're seeing a significant shift from the frantic pace of previous years. With 9,816 active listings currently available, buyers finally have the breathing room to be selective. This high inventory levels the playing field for anyone wondering, "should I sell my home before buying a new one?"

The dilemma usually boils down to two main fears. You either fear being stuck with two mortgages if your current home doesn't sell, or you worry about selling too quickly and having nowhere to go. In a market where the sales-to-active listings ratio is 11 percent, the "homelessness" risk is often mitigated by the sheer volume of available properties. However, the financial risk of overextending remains real if your sale price doesn't meet expectations. Understanding the real estate transaction process is the first step in managing these variables effectively.

Understanding Market Cycles in BC: Buyer’s vs. Seller’s Market

Leverage isn't uniform across the Valley. While the overall region favors buyers, specific neighborhoods like Willoughby in Langley or certain pockets of Surrey can behave differently. In these areas, townhomes might still move faster than detached homes in Mission. When you're in a buyer's market, selling first is often the safer bet because finding a new home is easier than finding a buyer for your old one. You can dive deeper into these localized trends in our Abbotsford housing market guide to see how inventory levels impact your specific street.

The Financial Stakes: Equity, Mortgages, and Moving Costs

Your "Net Proceeds" are the heartbeat of this decision. This is the amount left over after paying off your existing mortgage, commissions, and legal fees. With five-year fixed mortgage rates hovering around 4.04 percent to 4.09 percent in May 2026, your buying power is more stable than in recent years, but it isn't infinite. Before you commit to a purchase, you need a clear picture of your current asset's worth. A professional Home Evaluation provides the data you need to set a realistic budget. It helps answer the fundamental question: should I sell my home before buying a new one based on my actual equity? Knowing your numbers allows you to write offers with confidence, whether you choose to sell first or buy first.

Selling Your Home First: The Path of Financial Certainty

Selling your home first is the safest route to a stress-free move. It's the strategy we recommend for anyone who wants to avoid the "double mortgage" trap. When you ask yourself, "should I sell my home before buying a new one," consider the power of certainty. You won't be guessing about your net proceeds. You will have a firm dollar amount to bring to your next purchase. This approach turns you into a highly attractive buyer in the eyes of other sellers. It's about taking control of your timeline rather than letting the market dictate your stress levels.

Our team sees many homeowners find peace in this path. It eliminates the pressure to accept a lowball offer on your current asset just because you've already committed to another property. You can wait for the right buyer who appreciates the value of your home. This strategy allows you to focus on maximizing your sale price without the ticking clock of a second closing date hanging over your head.

Advantages: Budget Precision and Negotiating Power

One of the biggest hurdles in a modern transaction is the "Subject to Sale" condition. In the 2026 market, sellers in high-demand areas like Chilliwack or Abbotsford prefer clean, firm offers. If you've already sold your home in Langley, you effectively become a "cash buyer." You can negotiate harder on the price of your new home because you offer a guaranteed closing date. This leverage is invaluable when competing for rare detached properties. Beyond just the sale price, understanding the tax implications of selling your home ensures you keep as much of that hard-earned equity as possible. Having your finances fully settled allows you to move with confidence and speed.

The Interim Housing Challenge in the Fraser Valley

The main drawback to selling first is the logistical gap. If your home sells in 37 days, which was the April 2026 average for detached homes, but your new home isn't ready for months, you need a plan. Short-term rentals in Surrey and Langley are available, but they can be costly and require an extra move. We often suggest negotiating a "Rent-Back" agreement. This allows you to stay in your sold home for a few extra weeks as a tenant. It gives you a smoother transition and saves you from the true cost of double-moving, such as storage fees and professional movers. It's a simple solution that bridges the gap while you finalize your next chapter. If you're ready to see what your current home could fetch in today's market, a professional Home Evaluation is your best starting point.

Buying Your New Home First: For the Inventory-Conscious Mover

Sometimes, the perfect property appears before you've even cleared out your garage. In quieter Fraser Valley markets like Hope or Mission, unique detached homes or specific acreages don't hit the Multiple Listing Service every day. If you wait to list your current place, that dream home might be gone by the time you're ready to offer. This is the primary reason some homeowners choose to buy first. It's a move driven by inventory rather than immediate financial liquidity. While it carries more risk, it ensures you don't settle for a "good enough" home because you're in a rush to find housing after a quick sale.

We often see this strategy used by families looking for a very specific lifestyle change. When you're asking "should I sell my home before buying a new one," the answer might be "buy first" if you prioritize the property over the process. However, this path requires a solid backup plan and a clear understanding of your carrying costs. With the current average of 37 days on market for detached homes, you need to be prepared for the possibility that your current asset won't sell overnight.

The "Subject to Sale" Clause: How It Works in BC

In British Columbia, the "Subject to Sale" clause is your primary safety net. This condition tells the seller you'll buy their home only if you successfully sell yours by a specific date. In the current buyer's market, where the sales-to-active listings ratio is 11 percent, sellers are more likely to entertain these offers than they were in the frantic years of 2021 or 2022. However, these clauses usually come with an "escape clause." This allows the seller to keep marketing their home. If they get another offer, you typically have 24 to 72 hours to remove your subjects or walk away. To make your conditional offer more attractive, consider offering a slightly higher price or a more flexible closing date that favors the seller.

Bridge Financing: Bridging the Gap Between Two Homes

If you find your dream home but your current one hasn't sold yet, bridge financing can save the day. A bridge loan is a short-term financial tool that allows you to use the equity in your current home to pay the down payment on the new one. These loans are usually meant for a period of 90 days or less. With current 5-year fixed mortgage rates around 4.04 percent to 4.09 percent, you should use a mortgage calculator to estimate the interest costs of carrying two properties. Always have a "Worst Case Scenario" plan. If your home doesn't sell within that 90-day window, you'll need to discuss long-term financing options with your lender to avoid financial overextension. We can help you draft a buying strategy that accounts for these timelines, ensuring your transition remains a positive experience.

The Presale Advantage: A Strategic "Third Way" for 2026

Many homeowners feel trapped by the binary choice of selling first or buying first. There is a strategic middle ground that often gets overlooked in the Fraser Valley. Presale condos and townhomes offer a unique "third way" to manage your transition. This path allows you to secure your future home today without the immediate pressure of moving out of your current one. It effectively decouples the buying and selling process, giving you an extended runway to plan your next move with precision.

When you're debating "should I sell my home before buying a new one," a presale provides a buffer that a typical resale home cannot. You might secure a contract for a new townhome in Willoughby today, but the completion date could be 18 to 36 months away. This timeline allows you to stay in your current detached home while its value potentially stabilizes or grows. It's a forward-thinking strategy that leverages time as an asset. Working with a Presale Development specialist ensures you understand the nuances of these contracts and how they fit into your long-term wealth plan.

Why Presales are the Ultimate "Buy First" Strategy

The beauty of a presale is the fixed completion date. Unlike a resale transaction where you might have only 60 days to pack, a presale gives you years to prepare. You don't need bridge financing because you aren't carrying two mortgages at once. You only need to manage the deposit structure, which is typically spread out over several months. This financial breathing room is perfect for families who want to lock in a price in a stabilizing market. You can explore current developments in high-growth areas like North Delta to see what fits your lifestyle. It's about securing your spot in the neighborhood you want without the stress of an immediate relocation.

Risks and Rewards of the Presale Buffer

While the buffer is a major benefit, you must account for market fluctuations. In May 2026, we see benchmark prices for single-family homes at $1,374,800, which is down 8.8 percent from the previous year. However, prices have shown slight month-over-month increases for two consecutive months. This suggests a potential stabilization. Your goal is to ensure your current home maintains its value so that when completion day arrives, your equity is ready to be deployed. A professional contract review is vital here, especially regarding assignment clauses. These clauses allow you to sell your contract before completion if your plans change. If you want to see how this strategy aligns with your specific goals, connect with our team to discuss upcoming projects.

Developing Your Transition Strategy: A 5-Step Action Plan

Execution is where your research turns into reality. You've weighed the pros and cons of each path, but a successful move requires a structured approach. To answer the question, "should I sell my home before buying a new one," you need a plan that accounts for the current 2026 Fraser Valley climate. Follow these five steps to ensure a seamless transition with minimal financial risk.

- Step 1: Confirm Your Buying Power. Get a professional Home Evaluation. This isn't just a guess; it's a data-backed assessment of your net proceeds after commissions and fees.

- Step 2: Analyze Local Inventory. With 9,816 active listings currently in the Valley, you need to know if your target home type is in high demand or sitting on the market.

- Step 3: Validate Your Financing. Speak with a broker about bridge loan eligibility. Knowing you have this safety net changes your entire approach to writing offers.

- Step 4: Establish Your Risk Floor. Decide if you'll sell first for total certainty, buy first to secure a rare property, or choose a presale for the extended buffer.

- Step 5: Assemble Your Team. Partner with professionals who understand both sides of the Langley, Surrey, and Abbotsford markets to coordinate your dates.

The Importance of a Comparative Market Analysis (CMA)

A listing price is just a number on a screen. An actual sale price is what pays your next down payment. Steve Kooner & Associates uses a deep-dive Comparative Market Analysis to bridge this gap. We look at the 37-day average for detached homes and the 11 percent sales-to-active ratio to predict exactly how long your home will take to sell. We identify the "Sweet Spot" for pricing. This ensures you don't stay on the market too long while your new home's closing date approaches. It's about using real-time data to protect your equity.

Why a Local Agent is Your Best Insurance Policy

BC real estate contracts are complex. One missing clause can cost thousands in interim housing or bridge interest. A local expert acts as your insurance policy against timing errors and financial overextension. We often have access to off-market opportunities that can solve your timing dilemma before a home even hits the MLS. Our team is committed to taking the stress off your shoulders through every negotiation. If you're ready to master the timing of your move, contact our team for a personalized strategy session. Let's make your 2026 move your most successful one yet.

Master Your Fraser Valley Transition with Confidence

Your next chapter in the Fraser Valley should be defined by excitement, not logistical stress. We've explored how the 2026 market reality of high inventory provides a unique cushion for your decisions. Whether you choose the financial certainty of selling first or the strategic buffer of a presale, the key is a personalized plan. Deciding should I sell my home before buying a new one is a major milestone, and you don't have to navigate it alone. Each neighborhood, from Mission to North Delta, requires a specific approach based on real-time data.

With over 20 years of Fraser Valley expertise and top-tier representation at Royal LePage Wolstencroft, our team brings a wealth of local knowledge to your side. We specialize in everything from complex relocation services to identifying the best new construction opportunities. Our goal is to ensure your asset is protected while you secure the perfect property for your family's future. We're here to act as your partners, taking the weight of the transaction off your shoulders.

Get Your Free 2026 Home Evaluation and Move Strategy today. Let's turn your real estate goals into a seamless reality and move you forward with total peace of mind.

Frequently Asked Questions

Can I buy a home before selling my current one if I don’t have a massive down payment?

You can buy before selling by leveraging the equity in your current property through bridge financing or a Home Equity Line of Credit (HELOC). This allows you to access your down payment funds without having the liquid cash on hand. Most lenders in BC require a firm sale agreement on your current property to approve a bridge loan. This ensures you have a guaranteed exit strategy and aren't carrying two debts indefinitely.

What happens if my home doesn’t sell before the completion date of my new house?

If your home remains unsold by the completion date, you'll likely need to secure long-term financing for both properties or negotiate a completion extension with the seller. This scenario is the primary risk for anyone wondering, "should I sell my home before buying a new one." In a market where detached homes currently average 37 days to sell, it's vital to have a backup plan. This might include a temporary price reduction to trigger a faster sale or a short-term rental strategy.

How long does bridge financing usually last in British Columbia?

Bridge financing in British Columbia typically lasts between 30 and 90 days. It's a short-term tool designed specifically to cover the gap between your purchase date and your eventual sale date. Lenders usually charge a higher interest rate for this convenience compared to a standard mortgage. You should also budget for administrative and legal fees, which typically range from $800 to $1,500 depending on the complexity of the transaction.

Is it better to sell first in a buyer’s market or a seller’s market?

Selling first is significantly safer in a buyer's market, like the Fraser Valley in May 2026. With 9,816 active listings available, finding your next home is much easier than finding a buyer for your current one. In a seller's market, you might secure a home first to avoid being left with no inventory. However, selling first in the current 11 percent sales-to-active ratio environment protects you from being forced into a lowball sale price later.

Does a "Subject to Sale" offer make me less competitive in Langley?

A "Subject to Sale" offer is naturally less competitive than a firm offer, particularly in high-demand Langley pockets like Willoughby. Sellers prefer the certainty of a deal that isn't dependent on your buyer's financing or inspection. However, because inventory is currently 45 percent above the 10-year seasonal average, many sellers are more willing to accept these conditions than in previous years. We can help you add incentives, like a flexible closing date, to make your conditional offer more attractive.

Are there tax implications for owning two primary residences for a short period?

You can generally own two primary residences for a short overlap without major tax penalties thanks to the Principal Residence Exemption. The CRA's "plus one" rule is designed to help homeowners who are transitioning between properties in the same year. If you decide to keep your first home as a long-term investment or rental property, the tax situation changes significantly. It's always best to consult with a BC tax professional to ensure you're meeting all provincial requirements.

What are the benefits of buying a presale home when I already own a house?

Buying a presale allows you to secure your future home at today's price while staying in your current house for another 18 to 36 months. This extended timeline removes the immediate pressure of a 60-day move and allows your current equity to potentially grow. You don't have to worry about bridge financing or carrying two mortgages until the new development is actually completed. It's a strategic way to plan a move without the typical stress of matching up two closing dates.

How do I calculate how much equity I can actually use for my next purchase?

To find your usable equity, start with a professional valuation of your home's current market value and subtract your mortgage balance, legal fees, and commissions. For example, with the current detached benchmark price at $1,374,800, your gross equity might look high on paper. However, your "buy power" is the net amount left after all closing costs are settled. We provide a detailed breakdown during our strategy sessions to ensure you don't overextend yourself on your next bid.

Disclaimer

"Not intended to solicit buyers or sellers that are under current agency agreement" "Each RE/MAX office is independently owned and operated"